Ten Wall Street Blogs You Need To Bookmark Now. David Wiedner, WSJ. Not on there yet. Maybe next year.

Resistance is futile: Why buy-and-hold beats value investing. Pop Economics. The market may or may not be efficient in some philosophical or theoretical sense, but to YOU, owner of a Schwab account and more gonads than grey matter, it probably is efficient. Cruelly so.

Two Points on Greece and CDS from felix: here and here. At risk of referencing pop culture and murdering a few metaphors, Credit Default Swaps don't kill people, and kvetching about CDS's role in the financial meltdown is a little bit like complaining that guns kill people during wars.

Jeff's Intermediate Micro Course. Because we all had so much fun drawing lines on white boards and then shifting and rotating them.

Thursday, February 25, 2010

Sunday, February 21, 2010

2.21.10 Marginal Propensity to Peruse

Going on Tilt: What Will Stop Chindia’s Growth? Kedrosky.

Why is Latin America poor? More evidence for coercion and commodities.

Reality be Damned. Unraveling the Chicago School of Economics.

Why export growth isn't a necessary condition for a sustained expansion. Worthwhile Canadian Initiative.

Ummm, Dr. Krugman? Modeled Behavior.

Revealed: Goldman Sachs’ mega-deal for Greece. From 2003, as recently re-reported by everybody else, poorly.

Invincible Markets Hypothesis. Rajiv Sethi

estimated multipliers for portions of the ARRA

d squared on when to trust a statistics major

Context may diminish art appreciation, especially for modern art.

Why was the industrial revolution British? all economics.

Why is Latin America poor? More evidence for coercion and commodities.

Reality be Damned. Unraveling the Chicago School of Economics.

Why export growth isn't a necessary condition for a sustained expansion. Worthwhile Canadian Initiative.

Ummm, Dr. Krugman? Modeled Behavior.

Revealed: Goldman Sachs’ mega-deal for Greece. From 2003, as recently re-reported by everybody else, poorly.

Invincible Markets Hypothesis. Rajiv Sethi

estimated multipliers for portions of the ARRA

{kind=link}

d squared on when to trust a statistics major

Context may diminish art appreciation, especially for modern art.

Why was the industrial revolution British? all economics.

Friday, February 12, 2010

02.12.10 "Its major role is to transform the forms of wealth that exist in the economy into forms of wealth that savers want to hold."

Our title today is from an off hand comment that Brad DeLong made (in subsection 5). It is worth quoting at length, as it seems to be a good summary of "the money markets" which I suspect we will be getting into shortly:

Inventory cycle and GDP. Calculated Risk. A wonderful illustration of overinvestment in inventories.

Economists' Hubris - The Case of Risk Management. SSRN. Yet another in the ongoing series of "models are guidelines."

Microlender Accion USA Avoids 'Antipoverty' Pitch. American Banker (H/T Felix, i think).

Paying Zero for Public Services. WorldBank

The Nordics in the global crisis . VoxEu

An Interview with Paul Samuelson. New Yorker.

Time to go read the Macro Chapter 4.

The financial-monetary sector does a lot more than facilitate exchange--a problem that was solved by the invention of coinage under Gyges King of Lydia 2800 years ago. The financial-monetary structure does facilitate exchange, but that is only one of its roles. Its major role is to transform the forms of wealth that exist in the economy into forms of wealth that savers want to hold. The forms of wealth that exist in the economy are long-term illiquid risky projects and organizations that require a good deal of supervision and oversight. The forms of wealth that savers want to hold are short-term liquid safe assets that can be left to manage themselves. To move from one to the other financiers must (a) find people tolerant of bearing risk, (b) people willing to monitor and oversee, (c) people to make markets to create liquidity, while (d) betting that the law of large numbers can keep the whole thing from crashing down as they try to maximize their profits by paying the minimum to outside risk bearers, monitors, and market-makers.

Inventory cycle and GDP. Calculated Risk. A wonderful illustration of overinvestment in inventories.

Economists' Hubris - The Case of Risk Management. SSRN. Yet another in the ongoing series of "models are guidelines."

Microlender Accion USA Avoids 'Antipoverty' Pitch. American Banker (H/T Felix, i think).

Paying Zero for Public Services. WorldBank

The Nordics in the global crisis . VoxEu

An Interview with Paul Samuelson. New Yorker.

Time to go read the Macro Chapter 4.

Tuesday, February 9, 2010

02.09.10 Scientifical Learnings of Kazachian Macroeconomists for Make Benefit Glorious Nation of America

The title of today's blog post comes from the byline of The Money Demand, who links to three posts on the EMH

More from Scott Sumner on the EMH

Which leads me to post my favorite chart on the supply and demand of EMH:

From: The supply and demand for (belief in) EMH

Markets, in general, reflect all available information because people don't believe that they can figure out something that the market doesn't know. This has different implications for an asset manager than it does for a central banker.

In which I read more of Brad DeLong's back catalogue: The Triumph of Monetarism? which is a great history of whatever war we pretend Monetarism and Keynesian to be in.

Profits are Good. Falkenblog.

More from Scott Sumner on the EMH

Which leads me to post my favorite chart on the supply and demand of EMH:

From: The supply and demand for (belief in) EMH

The downward-sloping (hence "demand") curve shows the extent to which EMH is true as a function of the extent to which people believe EMH is true. At one extreme, if nobody believes that EMH is true, so people believe there is no relation between market prices and fundamental values, then each individual has a strong incentive to research carefully the fundamental values of assets before buying and selling, and so market prices will reflect all the information available to everyone, so EMH will be true. At the other extreme, if everyone believes EMH is true, so that market prices already reflect all available information on fundamental values, then no individual has any incentive to collect and process that information, and everybody picks assets by throwing darts, or buys the index, so market prices will not reflect any available information on fundamentals, so EMH will be false.

Markets, in general, reflect all available information because people don't believe that they can figure out something that the market doesn't know. This has different implications for an asset manager than it does for a central banker.

In which I read more of Brad DeLong's back catalogue: The Triumph of Monetarism? which is a great history of whatever war we pretend Monetarism and Keynesian to be in.

Profits are Good. Falkenblog.

Monday, February 8, 2010

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Sunday, February 7, 2010

02.07.10 Post-Modern Theories of Central Banks

Interest rate targeting as a social construction. Worthwhile Canadian Initiative. Up next, Lacanian Mirror State and the Flow of Funds Model.

d short's newest graph: The Road To Recovery. d short.

Is the International Role of the Dollar Changing? NY Fed.

For the marketing majors: What's more persuasive: fiction or non-fiction? Barking up the wrong tree. The takeaway: Bonding with characters makes people lower their guard.

When you can deduct the cost of your MBA. NYTimes

If a 10-pound note is lying on the ground in Davos, will a billionaire pick it up?

An Historical Look at the Budget

Brad DeLong linked to a very old post he did about the Keynesian Counter Revolution, which basically melded both Monetary Theory and Keynesian Theory, but the site is intermittent.

d short's newest graph: The Road To Recovery. d short.

{kind=link}

Is the International Role of the Dollar Changing? NY Fed.

For the marketing majors: What's more persuasive: fiction or non-fiction? Barking up the wrong tree. The takeaway: Bonding with characters makes people lower their guard.

When you can deduct the cost of your MBA. NYTimes

If a 10-pound note is lying on the ground in Davos, will a billionaire pick it up?

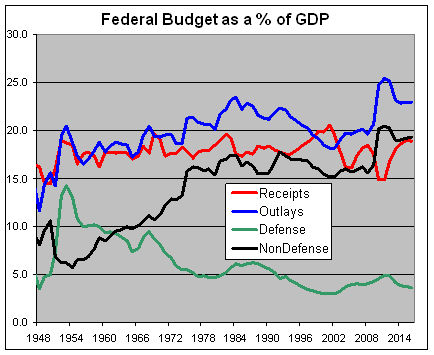

An Historical Look at the Budget

Brad DeLong linked to a very old post he did about the Keynesian Counter Revolution, which basically melded both Monetary Theory and Keynesian Theory, but the site is intermittent.

Saturday, February 6, 2010

02.06.10 The proper spread on a proper pint

Articles from the WSJ, as suggested by professor Blakely:

Mon. 2/1

“Deficit to Hit All-Time High”

“Obama to Skip Annual EU Summit”

“Emerging States Lead Dados Talk”

“The Ticker”

Tues. 2/2

“Data Hit Hopeful Notes for Economy”

“Deficit Balloons Into National-Security Threat”

“U.S. Move Sows Confusion in EU”

“Deficit Policy: Waiting for Growth”

Wed. 2/3

“Home Ownership Rate Declines”

“China Bank Slapped”

“Australian Bank’s Rate Call Reflects Chinese Influence”

Thurs. 2/4

“EU Warily Support Greece’s Deficit-Reduction Plan”

“Bernanke’s Exit Strategy: Tighter Reserve Requirements”

“Painful Productivity Pickup Promises Payoff”

Fri. 2/5

“Global Markets Shudder”

“Cost of Insuring Debt Alarms Investors”

“Debt Crunch Pressures Euro”

“Rising U.S. Job Worries Add to Upheaval”

“China Escalates Fight Over Western Tarrifs”

“Sovereign Risk Meets Sovereign Reality”

Sat. 2/6

“Signs of Hope as Jobless Rate Falls”

“Opinions Split on Job Creation”

“Consumers Keep Brakes on Borrowing”

“China’s Export Focus Breeds Backlash”

“Euro Drops on Debt Worries”

Update. The economist links for this week:

Geopolitics: Facing up to China

America’s budget: Clueless in Washington

Argentina’s reserves: Central Bank robbery

Greece’s sovereign-debt crisis: A very European crisis

Buttonwood: Stimulating debate

Mon. 2/1

“Deficit to Hit All-Time High”

“Obama to Skip Annual EU Summit”

“Emerging States Lead Dados Talk”

“The Ticker”

Tues. 2/2

“Data Hit Hopeful Notes for Economy”

“Deficit Balloons Into National-Security Threat”

“U.S. Move Sows Confusion in EU”

“Deficit Policy: Waiting for Growth”

Wed. 2/3

“Home Ownership Rate Declines”

“China Bank Slapped”

“Australian Bank’s Rate Call Reflects Chinese Influence”

Thurs. 2/4

“EU Warily Support Greece’s Deficit-Reduction Plan”

“Bernanke’s Exit Strategy: Tighter Reserve Requirements”

“Painful Productivity Pickup Promises Payoff”

Fri. 2/5

“Global Markets Shudder”

“Cost of Insuring Debt Alarms Investors”

“Debt Crunch Pressures Euro”

“Rising U.S. Job Worries Add to Upheaval”

“China Escalates Fight Over Western Tarrifs”

“Sovereign Risk Meets Sovereign Reality”

Sat. 2/6

“Signs of Hope as Jobless Rate Falls”

“Opinions Split on Job Creation”

“Consumers Keep Brakes on Borrowing”

“China’s Export Focus Breeds Backlash”

“Euro Drops on Debt Worries”

Update. The economist links for this week:

Geopolitics: Facing up to China

America’s budget: Clueless in Washington

Argentina’s reserves: Central Bank robbery

Greece’s sovereign-debt crisis: A very European crisis

Buttonwood: Stimulating debate

Wednesday, February 3, 2010

2.03.10 "What we have here is a failure to communicate"

Notes from 6111 Geopolitics:

Doing Business, China

Doing Business, India

Bush administration puts forth trade pact with Columbia. Sep 25, 2006

Smoot Hawley Tariff Act. (wiki)

Misadventures of the Most Favored Nations. (Amazon)

Doing Business, China

Doing Business, India

Bush administration puts forth trade pact with Columbia. Sep 25, 2006

Smoot Hawley Tariff Act. (wiki)

Misadventures of the Most Favored Nations. (Amazon)

Monday, February 1, 2010

02.01.10 "This is a matter of law and economics, not politics."

Notes and links from 6111, geopolitics:

EDF on the TXU buyout by TPG

EU rejects GE bid for Honeywell. (cnn)

Time's analysis of the failure of the deal. (Time)

Case study from NYU. (NYU, .pdf)

THE ATTEMPTED MERGER BETWEEN GENERAL ELECTRIC AND HONEYWELL: A CASE STUDY OF TRANSATLANTIC CONFLICT. (Oxford Journals)

Bundling and the GE-Honeywell Merger. (SSRN)

An interview with Mario Monti

EDF on the TXU buyout by TPG

EU rejects GE bid for Honeywell. (cnn)

Time's analysis of the failure of the deal. (Time)

Case study from NYU. (NYU, .pdf)

THE ATTEMPTED MERGER BETWEEN GENERAL ELECTRIC AND HONEYWELL: A CASE STUDY OF TRANSATLANTIC CONFLICT. (Oxford Journals)

Bundling and the GE-Honeywell Merger. (SSRN)

An interview with Mario Monti

Subscribe to:

Posts (Atom)